The Full Story:

So far, 2023 has surprised investors with its buoyancy. Year to date, the S&P 500 has rallied over 6%, which sounds impressive, but less than the returns of some alternatives. Small-cap US stocks have rallied 8%, developed international stocks nearly 10%, and emerging market stocks almost 12%. Even bonds have begun generating returns again, with the Aggregate Bond index up 3.5% already. These returns have all eclipsed the flat-on-the-year consensus forecasts provided by Wall Street strategists–tune in for our 2023 forecast on February 16th. But for these returns to remain aloft requires inflation to cool, the economy to only slightly recess, and corporate earnings to provide resiliency. This week we received insights into the status of all three.

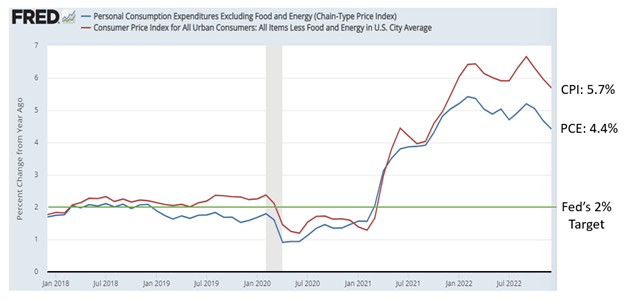

The Fed’s Favorite Inflation Evaluation

On Friday, the Bureau of Economic Analysis released its most current read on US inflation via the Personal Consumption Expenditures Index (PCE). This index differs from the Consumer Price Index (CPI) calculated by the Bureau of Labor Statistics. While the Consumer Price Index sources its data from consumers via household surveys, the PCE sources its data from suppliers. While the CPI only covers out-of-pocket expenses for consumers, the PCE includes payments on behalf of consumers by businesses and governments. This makes it somewhat less volatile, and a more comprehensive read on inflation, earning it the privilege of being the Fed’s preferred measure. Here are the most current readings on two indicators (food and energy):

Fortunately, the PCE inflation index registers lower current inflation than the CPI inflation index at 4.4% vs. 5.7%, respectively. Unfortunately, the Fed’s 2% target remains some distance away. Nonetheless, Friday’s cooler-than-expected reading added a lift to the markets and offered further evidence that inflation has decidedly tacked downward.

In 2022, the US Economy Grew on Queue

The US economy grew 2.9% in the 4th quarter. The growth registered .3% above expectations despite slowing .3% from its 3rd quarter gain. For the year, the US economy grew 2.1%, spot on with its long-term potential growth rate. However, given the Fed’s mission to cool the economy to douse inflation, these numbers appear perversely problematic. However, within the report, much of the gain in GDP stemmed from government spending, trade gains, and inventory builds. Consumers, which account for nearly 70% of GDP, continued to spend, but their spending pace clearly diminished into quarter’s end. Also, the sizable rise in inventories indicates decreasing demand, reducing the need to stockpile further into Q1. If you strip out gains from trade and inventories, US GDP only grew .8%, a much more innocuous read for the Fed. Overall, this positive report without any Fed moving surprises only adds further rally support.

Earnings Down, Surprises Up, Markets Up

While we have only completed 25% of the 4th quarter earnings season, numbers have largely arrived better than expected. While analysts expected a decline in S&P 500 earnings, the decline should be less than feared. Remember, it’s the spread between reality and expectations that moves markets more than reality itself, and 69% of reporting companies have beaten expectations. With 75% of the earnings season yet to go, it’s too early to declare victory. However, the reality of the market rallying through a season of earnings decline is not unprecedented. In fact, bear markets that accompany earnings declines tend to bottom six to nine months before the earnings themselves bottom. With the S&P October low intact, we think that would place the earnings nadir within the 1st half of 2023 right on queue. As long as something exogenous and unforeseen doesn’t clobber corporate earnings, “better than expected” adds rally support even as earnings decline.

Fed-ruary 1

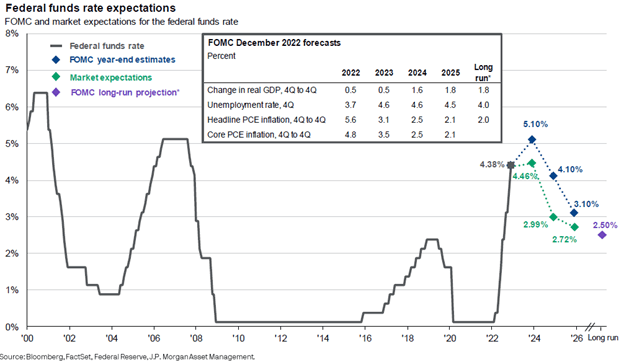

Next week the Fed will raise interest rates .25% to 4.75%. We expect to hear more hawkish refrains about rates being higher for longer, along with some slight acknowledgment that inflation has tempered. Markets will take this in stride as the data released matters more than the Fed’s rhetoric at this point. In fact, the market’s expectation for the Fed’s interest rate policy path now widely diverges from the Fed’s own forecast:

Markets now predict a rate cut by year-end while the Fed foresees adding a couple more increases. This difference of opinion will start pressuring the Fed to relent or lead them to double down on their rhetoric to bring markets to heel. The press conference next week should help with the reconciliation. We will be listening closely… and will report back!

Enjoy your Sunday!