The Full Story:

2022: The Fed vs. Investors

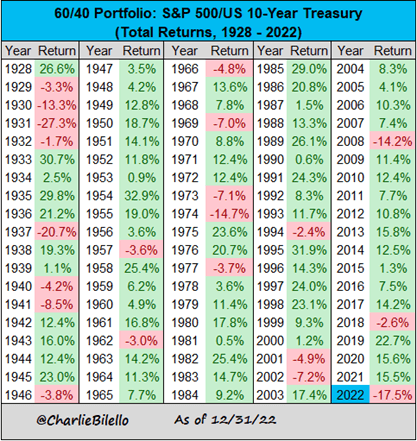

2022, adieu. You provided us with many wins and losses but mostly for investors, losses. Unfortunately, this was by design. As the year began, the Federal Reserve forcefully grabbed the baton and became the maestro of 2021’s overstimulated economic cacophony. They slammed the breaks on the money supply with historic rate hikes and historic asset sales. They wanted asset prices to fall. In response, Bitcoin fell 65%, Tesla 65%, Meta 64%, Netflix 51%, Google 39%, the Nasdaq 33%, the S&P 500 20%, the Aggregate Bond Index 13%, and even gold tarnished 1%. For traditional stock and bond investors, it was the worst year of returns since 1937:

![]()

Other asset classes that operate with a lag, like venture capital, private equity, and private debt, sharply marked down their values as well. Even housing prices found their way lower towards year-end. In short, only investors long in commodities stimulated by war profited in 2022. But that was last year.

2023: The Fed vs. Employers

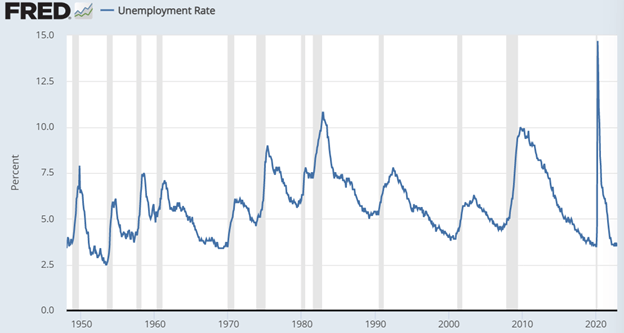

The Fed has a mandate from Congress to throttle the US economy to a pace that maintains price stability and maximum employment. With the US unemployment rate at historic lows, half of the Fed’s Congressional mandate has been met. But with inflation at 7% versus the Fed’s 2% target, half of the Fed’s Congressional mandate has not been completed. Therefore, the Fed has a constitutional obligation to lower price levels. Since stimulus over-throttling in response to COVID caused excessive demand per unit of supply, the Fed must diminish demand. Structurally, 70% of the US economy is consumer based. If you want to lower consumer demand, you must lower consumer wages. But while CPI inflation has fallen over the past six months by 2% from 9% to 7%, wage inflation at 5% hasn’t budged. Getting this number down below 3% is the Fed’s primary objective for 2023. As investors learned in 2022, what the Fed wants, the Fed gets. Unfortunately, a rapid wage decline likely requires a rapid increase in the unemployment rate, meaning the Fed’s mandate to lower inflation has become an employer mandate to fire workers. While it may appear that employers are not complying with the headline as the unemployment rate is pegged at historic lows (3.5%), leading employment data tells us a different story.

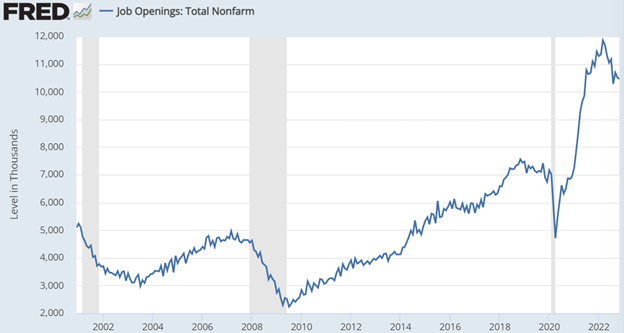

Job openings have declined:

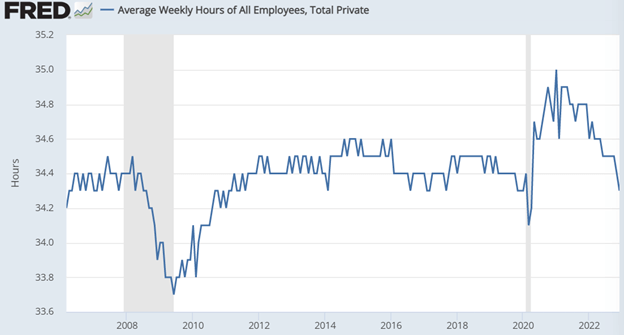

Weekly work hours per employee have declined:

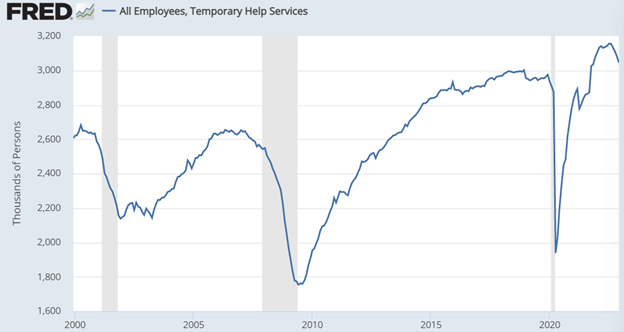

Temporary labor levels have declined:

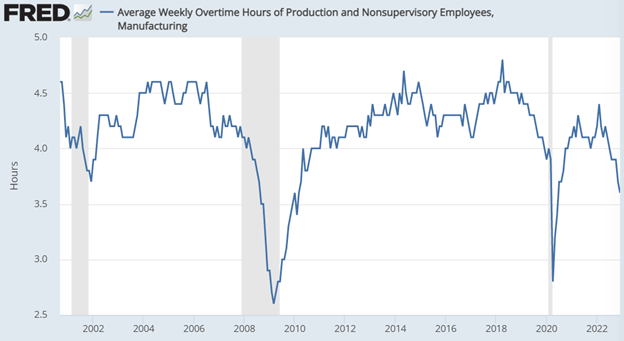

And overtime levels have declined:

So, while the lagging unemployment rate indicator remains hot, the leading unemployment indicators are cold. Employers have smartly begun complying with the Fed’s unemployment mandate; from here, it’s merely a question of pace. The faster employers shed labor and the faster wages fall, the sooner the Fed completes its disinflationary campaign. Therefore, the MOST IMPORTANT ECONOMIC INDICATOR FOR 2023 is the AVERAGE HOURLY EARNINGS report issued monthly by the Bureau of Labor Statistics (BLS). This report will arrive 12 times this year, on the first Friday of every month. Given the massive policy implications of each release, 2023 will feel like a 12-game playoff season for investors, with each release bound to drive significant upside or downside market volatility.

The first release, and therefore, the first wage playoff game results, arrived Friday morning. And the winner was… Investors!

Wage Playoff Game 1

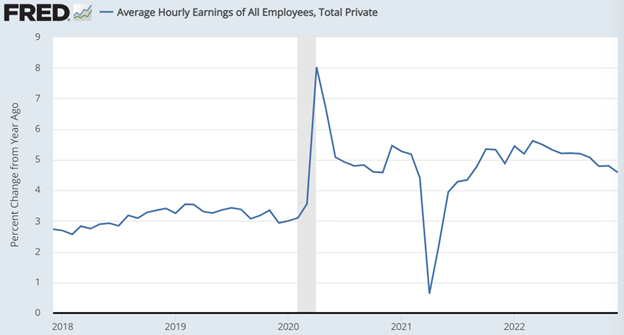

Average Hourly Earnings fell significantly in December from a previously reported 5.1% to 4.6%, well below the 5% anticipated by economists. Furthermore, the BLS downgraded November’s average hourly earnings gain from 5.1% to 4.8%. These numbers firmly establish a declining wage trend, as seen in the chart below:

Remember, the Fed wants this number below 3%, likely closer to 2.5%. We will get there faster if employers cut more high-wage jobs proportionally than low-wage jobs. Note the opposite dynamic in the chart above. When COVID quarantine mandates forced consumer services businesses closures (retail, restaurants, theatres, etc.), lower wage unemployment levels skyrocketed. With the rapid elimination of lower-wage workers, average hourly earnings spiked 5%, even as the unemployment rate spiked 10%! It’s possible the opposite could occur now.

Given the structural scarcity of service laborers, employers might prefer eliminating bureaucratic redundancies, technology overstaffing levels, and tenured underperformers proportionately more. If so, the surprise for 2023 could be that wages fall faster than expected, the Fed pivots faster than expected, unemployment rises less than expected, and markets rise instead of fall, contrary to the consensus. It’s possible. But it’s also a long playoff season, and we have 11 more games to go.

Series score to date: Bulls 1, Bears 0.

Have a great Sunday!