The Full Story:

Last week, we discussed how Federal Reserve Chairman Jerome “Pow-Pow” Powell predicted pain for the markets from his podium at Jackson Hole. While undefined, we interpreted his pain prediction as a call for 2 million job losses as his chosen mechanism for dousing inflation. This week, the Fed not only raised interest rates by .75% to 3.25%, but also overtly raised predictions for unemployment (pain). Markets reacted violently as the Fed’s true recessionary policy stance became inked. This week, we will walk through the details of the Fed’s Summary of Economic Projections released September 21st and translate what they have signaled about the state of play and the policy on tap:

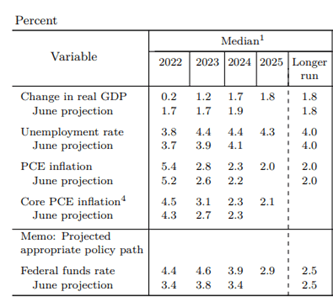

Economic Projections of Federal Reserve Board members and Federal Reserve Bank Presidents, September 2022

GDP: Downgrade

The Fed still projects that it can engineer a “soft landing” where economic supply and demand reclaim a non-inflationary balance without inflicting recession. Note that the Fed expects the economy to run below potential (1.8%) for the next three years, with 2022 marking a near zero growth rate for real GDP. For 2023, average growth projections accelerate to a meager 1.2% within a range of -.3% to 1.9%. From there, 2024 and 2025 appear more in line with potential. Takeaway: The Fed projects the economy to fumble through 2022 and limp through 2023 before reaccelerating to a below-average pace in 2024.

Unemployment: Downgrade

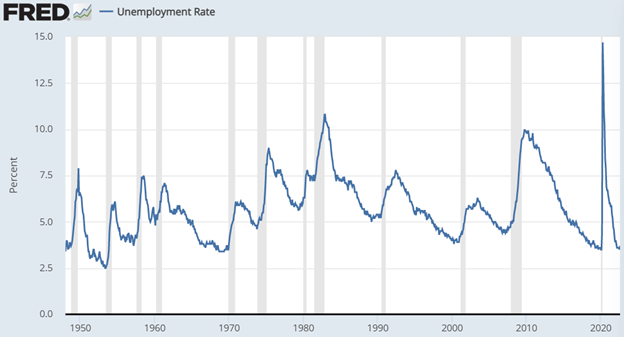

Last week, we proposed that the Fed would like to see the economy shed anywhere between 2 million and 5 million jobs to stifle inflationary wage pressures. Within the summary of economic projections, they didn’t quite signal that much “pain” to come at 4.4%, but the range of forecasts did top out at 5%. This translates into 1.2 million job losses to hit the midpoint (4.4%) and 2.1 million to hit the high point (5%). These numbers unnerved the markets more than any others released on Wednesday. While the Fed may hope for a GDP soft landing with moderate job losses, history doesn’t usually play out this way. When unemployment levitates, it tends to rocket higher as seen in the unemployment rate chart below:

Even a mild recessionary period like we experienced in 2001 saw a spike in the unemployment rate from 3.8% to 6.3%. Since the Fed has now explicitly targeted “unemployment” as the prescription for inflation, and since unemployment historically overshoots, these projections will likely prove optimistic. This makes corporate earnings projections seem optimistic as well, leading to the cascade of sale orders to end the week.

PCE and Core PCE Inflation: Downgrade

The Fed slightly increased their inflation projections for headline inflation to 5.4% this year, 2.8% next year and 2.3% for 2024. They also increased their core projections to 4.5%, 3.1% and 2.3%, respectively, against their 2% target. While these numbers nudged up slightly, it’s the slope that matters. The Fed feels confident they will conquer inflation and that rates will only decline from here. The market agrees as inflation expectation gauges remain anchored near similar levels. While higher unemployment levels and lower corporate earnings may be bad news for equity investors, lower inflation levels are actually good news. As inflation falls, interest rates tend to fall, relieving pressure on valuations. Therefore, while these levels are high, they are declining. The pace of the decline will determine future Fed policy and the pace of the market’s recovery.

Fed Funds Rate: Downgrade

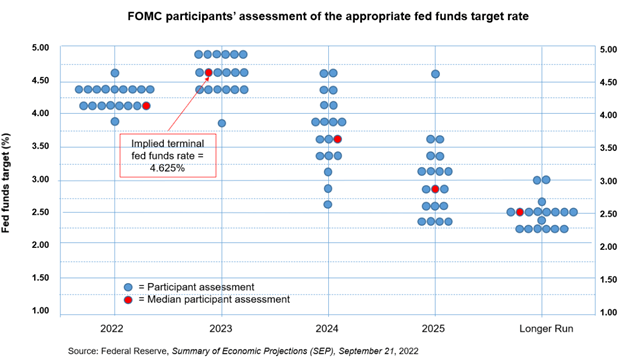

The Fed survey participants drastically increased their policy rate projections. The participants expect the Federal Funds rate to reach 4.4% by the end of 2022. This assumes another 1.25%-1.5% in rate hikes over the next three months! For 2023, the committee sees rates higher still at 4.6% before beginning their descent back to the 2.5% long-run target in 2024. Furthermore, examination of the dot plot (each survey respondents projection registers as a dot) suggests broad consensus around the heightened 2022 and 2023 rate levels as seen below:

That is high conviction in a highly restrictive policy. This did not go unnoticed by the markets as stocks plunged and rates spiked. This will also not go unnoticed by CFOs and HR departments. Expect bulk layoff announcements to accelerate. This is precisely what the Fed wants, and since unemployment levels tend to leap as groupthink takes hold, overshooting projections, we expect rate realities will undershoot projections.

Sentiment: Upgrade

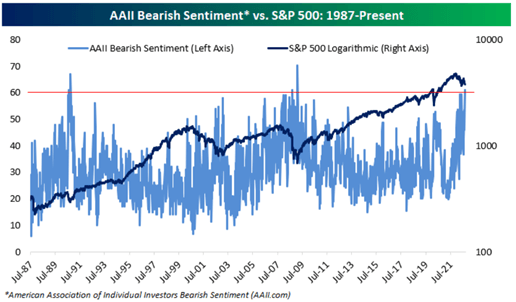

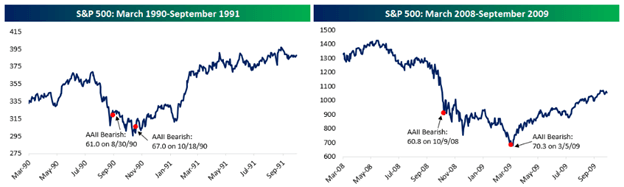

The dismal combination of the Fed’s projections did their job and has knocked the S&P 500 back toward its June lows. Consensus has turned decidedly and historically bearish. This week, 61% of individual investors (according to the American Association of Individual Investors) identified as “Bearish”. This has only happened a couple of times over the life of the survey as our friends at Bespoke investigated:

In the two other clustered occurrences, sentiment levels and overall market levels deteriorated even further before putting in durable bottoms within two to six months:

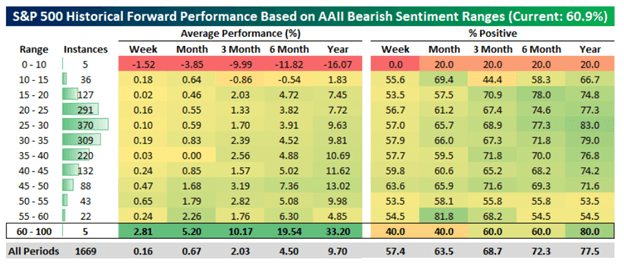

But…while readings of 60% could indicate more short-term pain for investors, the downfield results prove compelling for bargain hunters. Here are the forward returns from the full range of AAII Bearish sentiment readings:

Over the 5 similar periods of investor despondency, stocks returned 33% over the next 12 months, on average, with an 80% positive hit rate. This supports our base case that this is the bottoming phase for this cycle and should set us up within months for a positive 2023.

Here is the year end playbook:

- Continue harvesting tax losses wherever possible

- Reinvest proceeds to maintain market exposure

- Add cash weekly, or bi-weekly and be fully allocated by Halloween

- Should the market cascade lower between now and then, accelerate purchases

- Wait for history to rhyme!

Have a great Sunday!