The Full Story:

Markets rallied strongly off the June lows… is this just a bear market rally?

No. We believe inflation, long-term interest rates, and pessimism peaked in June. We predicted markets would appreciate 20%+ over the next twelve months after declining 24% from the January highs. What we did not expect was for it to happen in two months! Stocks used to take the stairs up and the elevator down. These days, it appears the elevator goes both ways.

At this point, the market has met technical resistance at its 200-day moving average (4300 on the S&P 500), and investor sentiment has returned to neutral. This sets us up for sideways action as we need more supportive data to backfill the rally, and the big uglies that would take us back to the June lows already reside in expectations. Inflation remains high, the Fed remains restrictive, recession seems inevitable, war bedevils Europe, Chinese lockdowns limit supply, earnings expectations are falling, etc. In the first half of 2022, this was news; in the second half, it is known. If the economy slides into slow growth and/or a shallow recession while inflation cools, there is no reason to plumb new lows. So, expect seasonal weakness into the mid-terms, but be fully invested by then. 2023 should look much better. That is our base case.

But isn’t this the 1970s?

No. In the 1970s, Nixon dropped the gold standard and told the Fed to figure it out. The Fed had no experience running monetary policy within a fiat system. They didn’t know which levers to pull and often had Congress pulling levers against them. The policy clumsiness of the 70s led to wild swings in price levels and an average CORE inflation rate of 6%+ for the entire decade. We peaked at 5.3% in February. July’s number released Friday fell to 4.3%. Forward-looking inflation expectations measuring out ten years predict inflation below 3%. This is not the 1970s.

What are your thoughts on Powell’s comments at Jackson Hole?

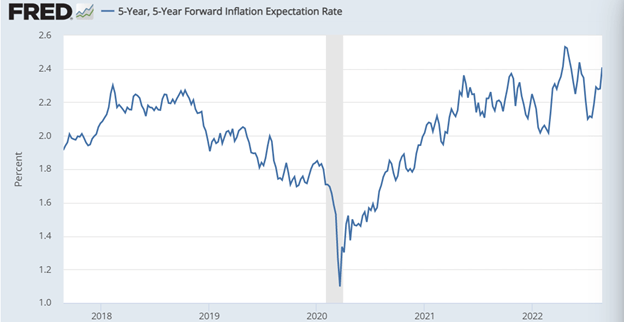

They surprised the markets, but they did not surprise us. Remember that the Fed has three primary policy tools: guidance, the Fed Funds rate, and balance sheet operations (QE/QT). Powell clearly calibrates guidance with inflation expectations, not current inflation readings. The market rally from the June lows also led to a reinflation of inflation expectations. When measuring inflation expectations, we focus on the 5-year, 5-year forward rate, which currently communicates inflation expectations for the 2027 to 2032 period.

Note that the decline we saw beginning in July accompanied the softening in the Fed’s forward guidance and the market’s rally. Now, with inflation expectations back on the rise, the Fed must strike a tougher tone. Powell needed to discipline markets at the Jackson Hole event. And so he did by inferring that a mild recession is preferable to inflation and that rates may need to be higher for longer, dispelling forecasts for a rate cut in Q1 2023. Powell played it right. Markets fell, but still closed 11% above the June lows.

How should investors position themselves going into year-end?

Longer-term investors must use the current volatility to take advantage of shorter-term traders. Sentiment-driven markets create mispricing that can lead to very attractive entry points. Consider this. Right now, 20% of the companies within the S&P 500 have a P/E ratio of less than 10. Five percent of the S&P 500 have a P/E ratio of less than 10, AND dividend yields above Treasuries! These include household names like JP Morgan and Intel. The investment values that trigger-happy traders unlock through forced selling create opportunity. For our investors, we have taken advantage of the mispricing by favoring dividend payers, value factors, smaller cap corporations, and international issues. We have shied away from higher P/E technology and consumer discretionary names, insulating us from the larger drawdowns. For investors, adding quality names at discounts today will pay off tomorrow. For traders, that is too long a time horizon. For them, the most directional leverage comes from areas like profitless tech and crypto markets. For the gamblers out there, firms like MicroStrategy represent both. Play with that if you like the action but focus the core of your efforts on more stalwart entities if you prefer reliable returns.

For cash holders, we continue to believe that markets will bounce within a range through Halloween and then track higher post-election. Dollar-cost-averaging over the next two months should establish an attractive cost basis. Should the market gap lower over that period…like they did on Friday…purchases should be accelerated.

Are you worried earnings estimates are too high?

I worry about everything! But I will point out that earnings grew 9% during the first half of the year while the economy technically recessed. The recession to come has been widely broadcast (deliberately), and CEOs have already reacted by trimming payrolls and expansion plans to preserve margins. While earnings may dip, we do not expect them to collapse.

Bottom line it for us

In sum, valuations have recovered quickly given the environmental switch from inflation to disinflation. Corporate earnings will soften along with the economy, but CEOs have had ample warning to adjust operations and preserve margins. The Fed has declared rates “neutral,” therefore recognizing that hikes from here will deliberately cause pain. They cannot soften their rhetoric, but we do expect them to soften their policy as pain prescribes.

Stay the course, buy dividends on the dips, and prepare for a more generous 2023.

Thank you, David.

Thanks for having me! (Or not)

Have a great Sunday!