The Full Story:

Of the 500 companies within the S&P 500, 467 have now reported second-quarter earnings. Recall that in the first quarter, S&P 500 companies managed to grow earnings by 10%, despite the 2% drop in GDP. With GDP contracting another 1% in the second quarter, could earnings defy gravity once again? Yes! Earnings are on pace to finish the second quarter up another 7%. Estimates for the third quarter and the 4th quarter also remain positive, with expected growth rates of 5.8% and 6.1%, respectively. For the full year of 2022, analysts expect earnings will grow 9%. These growth expectations coexist alongside clear recessionary signals like inverted yield curves and a negative turn in the leading economic indicators index. How do earnings grow…while the economy shrinks?

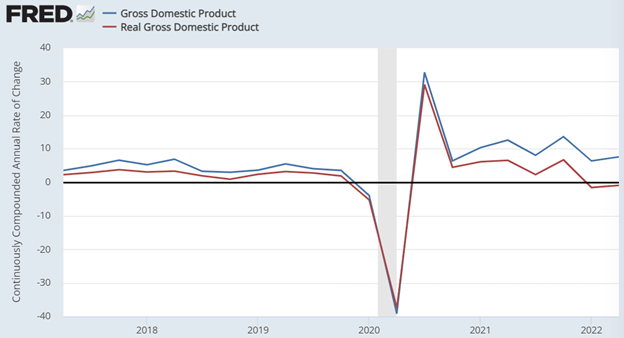

Real vs. Nominal

Economists speak of GDP net of inflation. They call this “real GDP.” Real GDP shrank 1.6% in the first quarter and .9% in the second. Economists do measure GDP gross of inflation as well. They call this “nominal GDP.” When inflation runs high, the spread between these two measures can grow quite large. For instance, without discounting GDP for inflation, “nominal GDP” grew 6.6% in the first quarter and 7.8% in the second! The chart below chronicles real and nominal GDP growth over the past five years. Remember, inflation alone accounts for the spread:

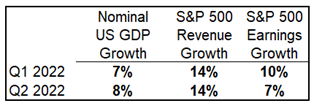

Things look very different when comparing the decline of “real GDP” with the above-average growth of “nominal GDP”. Fortunately for S&P 500 companies, they report their quarterly earnings in nominal terms, meaning they do not adjust their numbers for inflation. Therefore, the “nominal GDP” growth rate of the economy drives corporate financial reporting, not the “real GDP” growth rate. Level-setting the economy and corporations in “nominal” terms removes the dissidence:

When ignoring inflation, things across the economy and corporate releases look great! And while households factor in inflation when they spend their money, they don’t tend to factor it in when they count their money. Therefore, when it comes to reporting earnings, investment gains, and net worth, we all tend to live in nominal terms. Economists have a name for this as well. They call it the “money illusion.”

Economist Irving Fisher coined the term money illusion as a way of explaining people’s cognitive bias towards thinking in nominal rather than real terms. For example, across the economy, employees have received a “nominal” increase in average hourly earnings of 5% over the past year. Congratulations, employees! Unfortunately, “real” average hourly earnings decreased 2.7% over the past year. Therefore, in real terms, workers received compensation reductions, not increases. Congratulations, employers! The money illusion distorts appraisals and decision-making economy-wide. With high inflation, corporations can pass along sizable price increases to customers without adding any additional value. Many accredit the poor productivity growth in the 1970s economy to management’s nominal view, overappraisal of their financial performance, and lack of competitive investment. Today, as highlighted above, revenues grew 14% in the first and second quarters, with earnings growing 10% and 7%, respectively. Well done, corporate management! However, when we adjust for the GDP inflation factor and recast the numbers…

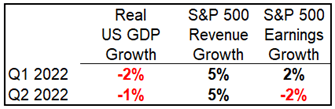

…things look materially worse. Real earnings over the last two quarters drop to 2% and -2%, respectively. Well, that’s a whole different story. Do better, corporate management!

Now it’s the Margins that Matter

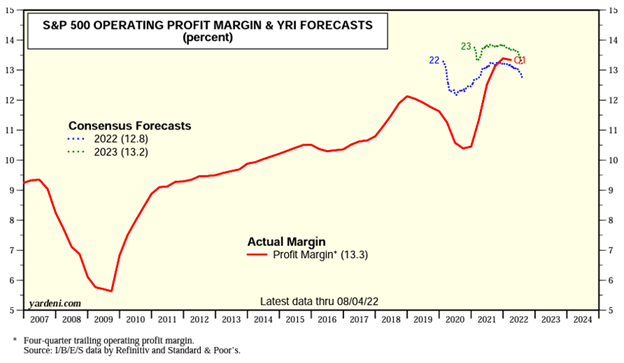

In normal economic times, the spread between real and nominal isn’t large enough to distort evaluations and decision-making. But with inflation high and growing more persistent, the money illusion and distortion risks take root. Those who feel comforted by inflation-powered revenue gains take note. As inflation abates, “false” revenue will recede with it. This will pressure management to trim expenses at pace to preserve margins. Tesla, JP Morgan, Amazon, Walmart, Netflix, Coinbase, Shopify, and a host of other companies have recently announced broad layoffs and austerity plans. While we have not yet seen a surprise uptick in the unemployment rate to date, we suspect it’s not far behind. Management, analysts, and investors must now shift focus away from “money illusion” earnings to purer measures like profit margins to properly appraise corporate performance. By the margins, management has well weathered the inflation storm to date, but things will get trickier from here as revenues get “real”!

Have a great Sunday!