The Full Story:

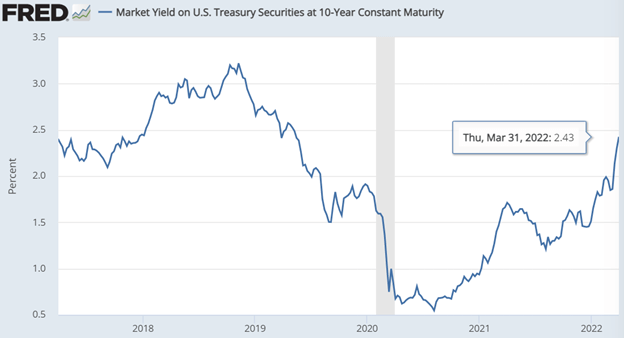

The first quarter has ended, and we could not be happier about it. Markets took blows from everywhere this quarter. Omicron re-quarantined businesses, the Fed raised rates, Putin invaded Ukraine, the yield curve inverted, and investor sentiment hit the canvas. Bond holders took the most pain. The Vanguard Total Bond Market Fund, with over $500 billion invested, fell 6% for the quarter versus 5% for the S&P 500. The dramatic moves in interest rates off the zero levels account for the declines:

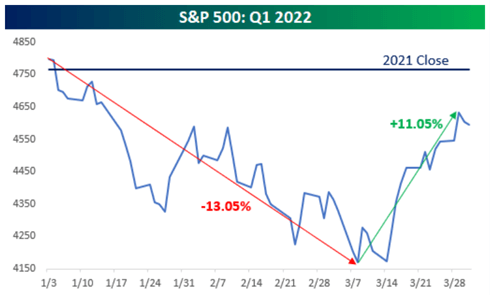

With inflation persisting and the Fed decidedly hawkish, interest rate sensitive bonds face even further headwinds. Credit sensitive bonds fared better, but still provided losses for investors with High Yield down 5% for the quarter. For the stock market, the quarter felt more like a year. The Powell/Putin punch combination battered the markets into early March, deeply depressing investor sentiment. Then, a stunning rally followed over the last two weeks of March, leaving the S&P 500 down a manageable 4.9% for the quarter overall:

Where Did that Rally Come From?

Despite 2022’s early turmoil, analysts expect earnings growth of 4.8% for the quarter and 9.4% for the year. For 2023, analysts forecast an additional 10% in earnings growth. As we discussed last week, inflation penalizes purchasers, but with wealth and income reservoirs overflowing, US consumers can withstand the price increases. Remember that inflation on its own doesn’t kill an economy. In the 1970s, GDP before inflation grew 9.9%, annualized. GDP after inflation grew 3.2%, annualized. For comparison, between 2010 and 2020, GDP before inflation grew 4%, while GDP after inflation grew 2.2% annualized. So, surprisingly, by the numbers, the 1970s economy outperformed!

While inflation may not kill an economy, it does lead to distortions, volatility, and policy risk. For example, the US economy suffered from three recessions in the 1970s as inflation averaged 6.7%. Between 2010 and 2020, inflation averaged 1.7% and the US economy did not recess. High inflation also leads to high uncertainty for investors and government officials alike, infecting decision-making. Just recently, the Fed has vacillated between gradual and dramatic rate hikes, while the Biden administration has vacillated between restricting oil production and subsidizing oil production. Inflated inflation leads to legislative volatility. Therefore, with inflation high, investors must become policy forecasters. With Biden’s approval rating at its lowest point, and Congress gridlocked entering the traditional mid-term handover, fiscal policy is effectively frozen. This leaves monetary policy in charge. Jerome Powell has big, complicated decisions to make, but the market’s forward inflation measures express confidence in him.

The Fed has not lost credibility as it did during the 1970s. Therefore, if you believe inflation will cycle lower as COVID and Putin fade, and if you believe Powell can restrain without recessing the US economy, earnings estimates will actualize, and markets will rally… just as they did to close out this quarter.

History Foretells Faith Rewarded

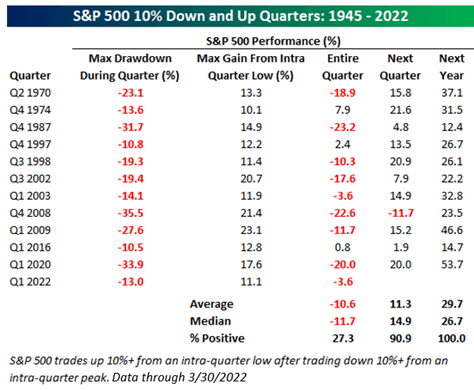

The Bespoke Investment Group provided some interesting context this week on bi-polar quarters like Q1 2022. Apparently, there have only been eleven quarters since WWII where we saw a 10% drawdown from a closing high followed by a 10% rally from an intraday low. Here are the stats on the eleven comparable occurrences and forward returns:

Historically, crazy quarters lead to crazy returns! Ten out of eleven times, the subsequent quarter generated positive returns for a 90% hit rate. Eleven out of eleven times, the subsequent year generated positive returns for a 100% hit rate, and those returns have been sizable. The median returns for subsequent quarters registered 14.9% and the median returns for subsequent years registered 26.7%. The quarters in the dataset also share obvious similarities.

In 1987 the market broke on Black Monday; investors lost faith, yet the economy and earnings ultimately prevailed. In 1998, the Asian Currency Crisis led to Russia’s technical default and the demise of Long Term Capital Management; investors lost faith, yet the economy and earnings ultimately prevailed. In 2009, the US financial system nearly collapsed; investors lost faith, yet the economy and earnings ultimately prevailed. In 2020, COVID shut down the world; investors lost faith, yet the economy and earnings ultimately prevailed. In 2022, COVID and Russian inflation forces have ravaged the world economy; will the economy and earnings prevail? Unclear… but based upon the dataset above, I like our chances.

Have a great Sunday!