The Full Story:

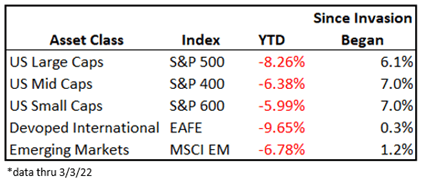

Since the Russian invasion began, oil prices have risen 20%, wheat prices have risen 20% and the 5-year breakeven inflation rate has risen from 3% to 3.2%. Putin’s initial strategy of bloodless coercion has devolved into a bloody incursion, which has not only stoked inflation but has also increased the risk of recession, financial crisis, and even nuclear engagement. Investor sentiment sits near historic lows and market volatility near panic highs. Here are the returns for various investable indices year-to-date and since the invasion began:

Surprisingly, since the invasion began, these major equity indices have traded flat to higher. Inside the data, we find two influences competing for prominence.

First, the

Year-to-Date (YTD)

returns favor lower valuations. The S&P 500 index has the highest valuation multiple, while US small caps and emerging markets have the lowest valuation multiples. Investors favor lower valuation asset classes during higher inflation and higher interest rate environments, explaining the performance differential. While valuations have declined since markets peaked on January 4th, the S&P 500 still trades for 19.1 times earnings while the S&P 600 trades for 13.7 times earnings and the MSCI Emerging Market Index trades for 11.9 times earnings. In an inflationary environment, lower P/E’s offer higher returns.

Second, the

Since Invasion Began

returns favor geographic distance from Russia. US companies have limited exposure to Russia, mostly through secondary effects. Higher inflation and supply chain issues threaten earnings, but US companies do little trading directly with Russia. The emerging market indices include Russia and therefore have taken the most direct hit as the Russian markets mark to zero. However, the majority of emerging market index holdings reside in Asia, which is relatively isolated from the disruptions. Furthermore, China carries the largest weight within the index and their disinterest in foreign affairs helps mitigate interruption risks. The largest direct linkages to Russia exist in Europe, which accounts for 65% of the EAFE index and explains the EAFE’s relative underperformance. In a Russian invasion environment, markets furthest away offer the highest returns.

Each of these influences has a strongman. Federal Reserve Chair Jerome Powell sets interest rate policy levels which inform valuation levels, while Russian Czar Putin sets geopolitical risk levels that inform sentiment levels. So far in 2022, each of these strongmen have spooked the markets into correction territory at different times. The S&P 500 fell 12% between January 4th and January 24th on concerns that Powell might willfully force the US economy into recession to douse inflation. For efficiency, let’s label the January 24th low of 4222 the “Powell low”. The S&P 500 then nearly fully recovered, only to have Putin’s aggression drive the S&P 500 down 12% again between February 9th and February 24th. For efficiency, let’s label the February 24th low of 4114 the “Putin low”.

On Wednesday of this week, Powell testified before Congress that he DOES NOT believe the economy needs to recess for inflation to clear. He disclosed his intent to raise interest rates .25% at the March meeting and that the Fed will continue tightening at a measured pace “as the data allows”. Importantly, he also handled himself with great composure on the hill, bolstering Fed credibility amidst the turbulence. From the 1/24 “Powell low” through Wednesday, the S&P 500 rallied 4% despite Putin’s deviance. Unfortunately, fears of nuclear fallout retracted 2% of the advance this week, but the “Powell low” remains intact, and his reassurances that killing inflation does not require killing economic growth adds measurable uplift beneath Putin’s downforce.

The conditions around Ukraine are unknowable. Putin’s campaign will kill innocents on both sides and destabilize markets until he retreats, negotiates peace, or topples. The longer it takes, the more damage he does. And yet, even with the escalation in violence and holocaust chatter, the 2/24 “Putin low” remains intact.

Therefore, in our assessment, Putin’s pugnaciousness becomes just another input into the Fed’s rate calculus. Markets are far more afraid of a Powell manufactured recession than Putin’s clumsy insurrection. It is Powell’s power that wields more lasting influence over market conditions, and his measured and supportive stance on Wednesday removed the larger risk. Putin may yearn to be a man of destiny, but for the global financial markets, he’s just an irritant.

Have a great Sunday!