The Full Story:

After smooth sailing in 2021, the recent market volatility has astute investors reopening their economic textbooks. The economic headlines do feel extreme: 7% inflation with 1.9% Interest rates, 6.9% GDP growth vs. 2% GDP growth potential, 25% corporate earnings despite 5.7% wage gains. Many of these numbers seem mismatched, making for volatile markets and volatile commentary. Further complicating matters, Jerome Powell and the Fed have completely flipped from super “we want inflation” doves to super “we want disinflation” hawks. Lastly, markets have pivoted from being highly correlated to loosely correlated, with powerful rotations, sector dispersions, and outsized moves on individual securities. If you are feeling a bit seasick to begin the year, you are not alone. However, when establishing investment expectations for 2022, the right question to ask is not “how many times will the Fed raise rates”, or “how high will the 10-year Treasury yield go”, or “will a skinny Build Back Better legislation pass the Senate”? If you want to know whether market returns will be positive or negative in any given year, simply ask… “are we heading into a recession”?

January Reality Below Expectations

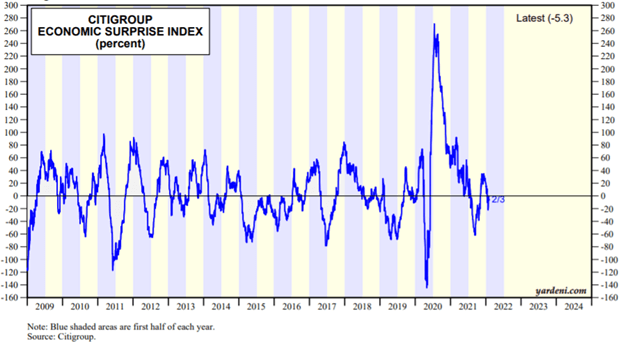

The Atlanta Fed publishes a real-time GDP forecast titled GDPNow. Its current forecast for first-quarter GDP growth is .1% versus the Blue Chip Economist’s estimates of over 3%. This has created some banter around recession risks on the year. Relatedly, the Economic Surprise Index, which measures whether economic reports meet, exceed, or fall short of expectations, has recently turned negative as seen below:

However, just because reports come in below expectations does not make them negative. As you can see, the Economic Surprise Index regularly oscillates between positive and negative readings. Furthermore, the Delta wave disrupted the economy in the third quarter of 2021, pressing GDP down to 2.3% from its 6%+ run rate. Likewise, the Omicron wave has suppressed January 2022 GDP given its even higher case counts and quarantines. However, we expect the Omicron disruption will pass much like the Delta disruption passed so we rely on more farsighted economic indicators for direction.

Follow the Lead

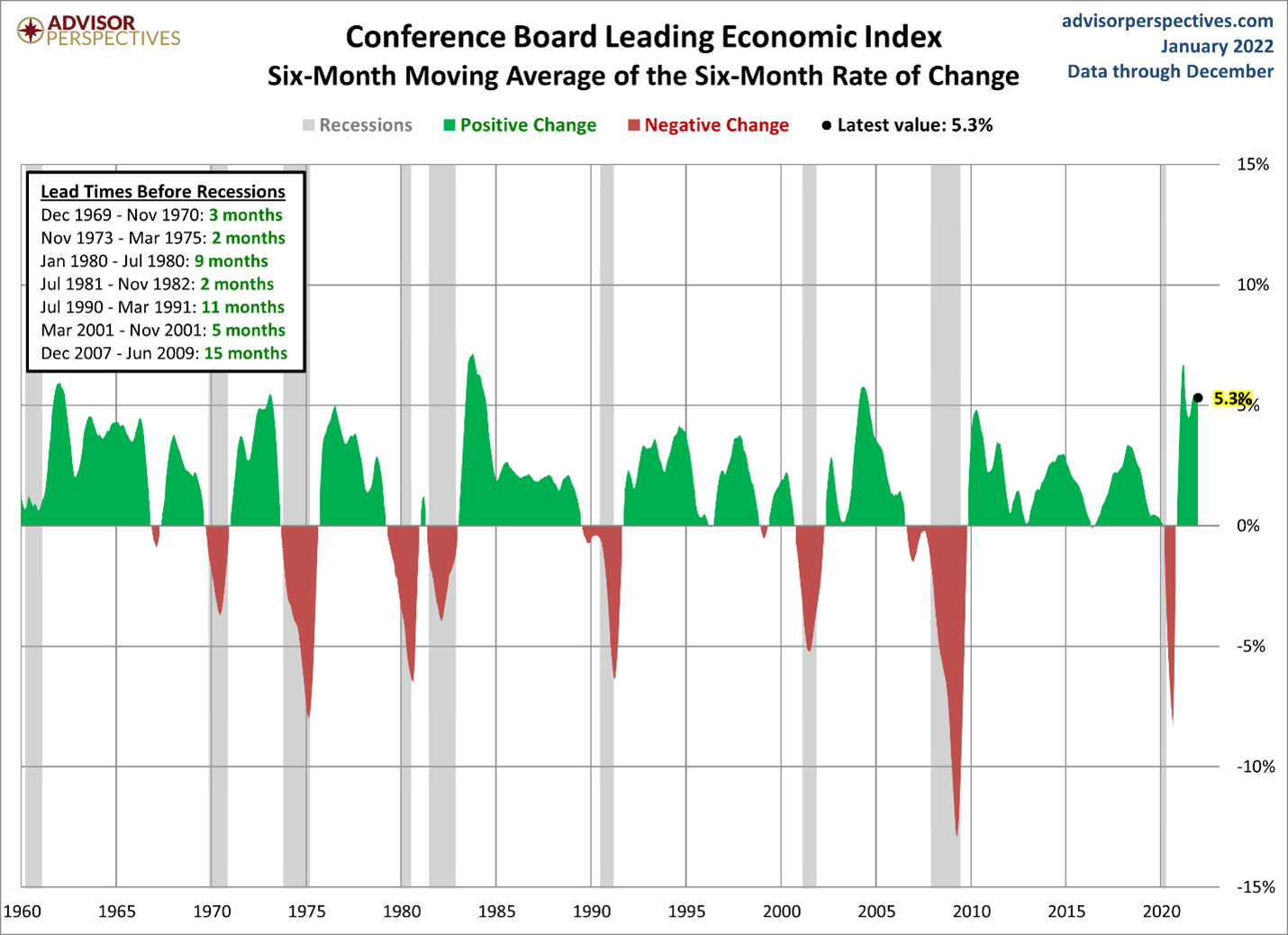

Each month, the Conference Board produces its index of leading economic indicators. The index follows 10 economic indicators and attributes the largest weightings to employment, monetary, and purchasing manager activities (movements in the S&P 500 only account for 3% of index weightings). Here is the current reading from the Conference Board’s Index of Leading Economic Indicators with recessions highlighted (we refer to the six-month moving average to smooth out variations):

Note that the current reading of 5.3% registers at the top-end of the range going all the way back to 1960. This suggests robust economic growth ahead. Also note that the indicator has a very strong track record for forecasting recessions in advance. Those of you following our commentaries in 2019 will recall that the swift decline in the index toward zero put us on recession watch and led us to apply hedges to our portfolios. Based upon the current readings, we see no such need. The index clearly signals robust economic conditions ahead.

Mind the Curve

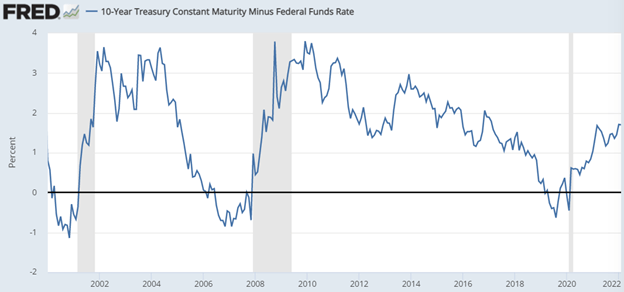

We also closely follow the shape of the interest rate curve as a recession harbinger. When long-term interest rates fall below short-term interest rates, banks lose the incentive to lend because they pay more on deposits than they make on loans. Since capital is oxygen for the economy, any reduction in capital leads to a corresponding reduction in economic activity. While the Fed has talked about raising rates, they haven’t yet, placing the slope of the yield curve in squarely positive territory:

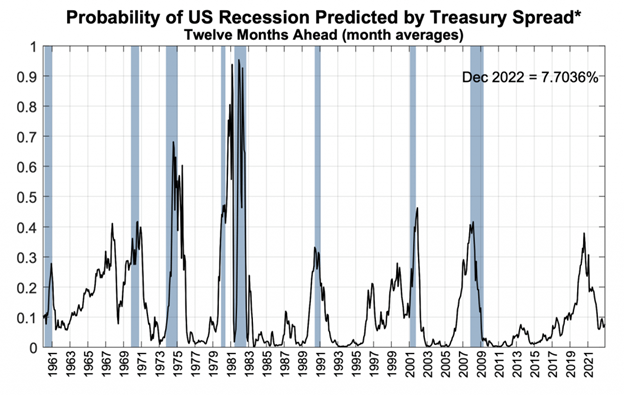

Recognize that the recent increase in longer term interest rates has actually improved the slope of the curve. This technically improves the economic outlook because banks have even more incentive to lend. Some forecasters prefer the 10-year minus 2-year curve given the “assumption” of rate hikes inherent in the 2-year yield. This curve shows some current risk of inverting. However, given our assumption that the Fed’s bark will be worse than its bite, the 2-year curve may overestimate the path for rate hikes and therefore understate its slope. Nonetheless, both yield curves are positive, leading the New York Fed’s own recession forecasters to assign low probabilities of near-term recession:

Given our working assumption that 2022 will not usher in a recession, equity investors should feel encouraged. Stock returns strongly correlate with corporate earnings and corporate earnings strongly correlate with economic growth. According to KKR’s Investment Strategy Group, since 1945 the S&P 500 has risen 88% of the time during years of economic expansion. Therefore, for the pessimists, markets have fallen 12% of the time during economic expansions, but only 4% of those declines exceeded 10%. So, losses in a rising economy are possible. They are just not probable. And when they occur, they are usually small.

Have a great Sunday!