The Full Story:

The Federal Reserve met this week and revealed their plan to reverse monetary policy in 2022. With inflation running high and unemployment running low, the shift was widely expected and appropriate. Markets reacted positively to the announcement and then negatively, then positively, and then negatively and positively again. With so many gyrations before and after the Fed meeting, how should investors prepare for 2022?

What the Fed Said

The Fed will increase their asset purchase reductions from $30 billion to $15 billion a month, effectively scheduling the termination of their COVID Quantitative Easing program this March. This means they will ONLY add $130 billion MORE in new money before stopping the printing press. When questioned on why they should bother to print at all, Powell gave an “easy does it” response.

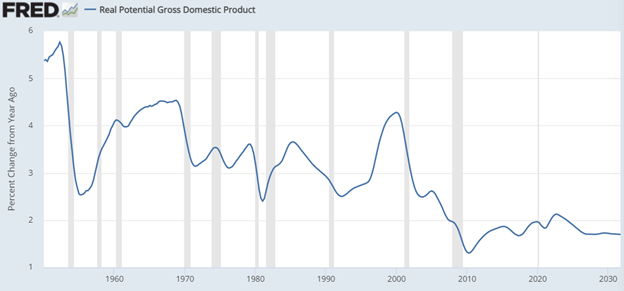

The Fed signaled their intent to increase interest rates .75% next year. Rate increases will begin once QE has ended. Since they tend to adjust rates at their quarterly meetings when they release projections, that would imply .25% in June, .25% in September and .25% in December. It is somewhat futile to look beyond that horizon given COVID and inflation uncertainties. Remember, without corresponding stimulus response, COVID is deflationary. Furthermore, the waning of existing stimulus is also deflationary. Recall also that our real potential GDP growth rate (productivity + workforce growth) sits below 2% due to demographic drags, which is also deflationary:

Therefore, while inflation has moved the Fed to act, it has done so conversationally (“we will keep printing money until March, then we will likely raise rates .75% after that”). That is hawkish in tone but dovish in practice. Furthermore, Powell mentioned at the press conference that they didn’t want to “upset” markets with their movements, implying that if the market boos they may rescript. I believe that they still believe the current inflation numbers will descend. That may mean fewer rate increases than projected. The surprise of 2022 may be the under on inflation, and the Fed’s response to it.

Should you Sell?

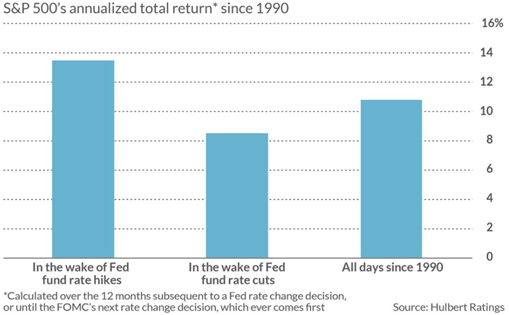

While I don’t think the Fed will raise rates up to its guess of 2.5% or so over the next 36 months, a rising rate regime has started. Fortunately, the Fed only raises rates to prevent the economy from “overheating.” When they projected rate hikes for next year, they also increased their real GDP growth expectations for 2022 from 3.8% to 4%. They also estimate 2022 inflation at 2.6%, making non-inflation adjusted or “nominal” GDP growth nearly 7%. This is a domestic revenue opportunity for corporations. Correspondingly, according to FactSet, S&P 500 companies should grow revenues by 7.5% next year and earnings should grow by 9.2%. Even if rates tick up slightly and crimp valuations, the earnings power should win out. This is not an unusual outcome. In fact, initial rate hikes have better performance track records than rate cuts:

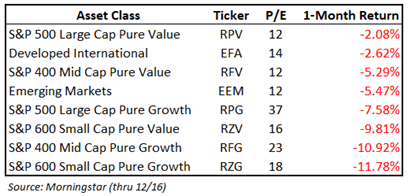

Therefore, investors should not sell in anticipation of rate hikes alone. However, they might want to reconsider what they own. Recall that higher P/E stocks have lower “earnings” yields (i.e., a P/E of 50 is the same as an earnings yield of 2%). As yields rise, the relative value of stock earnings yields declines. Therefore, high P/E stocks should be at a disadvantage to low P/E stocks when rates rise. Markets have sold off over the last month in anticipation of a hawkish pivot from the Fed. Let’s test our theory by comparing returns across different equity classes and valuation levels over the period:

In short, our first four contestants with an average P/E of 12.5x suffered 3.87% declines, while our bottom four contestants with an average P/E of 23.5x suffered 10.02% declines. Theory proven! Therefore, while rising rates (on their own) shouldn’t kill this bull market, investors may need to get more selective on which stocks they ride.

Have a great Sunday!

David S. Waddell

CEO, Chief Investment Strategist