The Full Story:

Last week we discussed in detail how interest rates relate to equity market valuations. In fact, we emphasized that the only valuation metrics worth paying attention to are the RELATIVE valuations between asset classes, predominately between stocks and bonds.

Today, 10-year Treasury bonds yield 1.56% and AAA corporate bonds yield 2.8%. The S&P 500 stock index has an earnings yield of 4.6% (Calculation = 1/current P/E ratio of 21.53). Since 4.6% is greater than 1.56% or 2.8%, stocks hold the valuation advantage and should, therefore, hold the return advantage.

To form, the Vanguard Total Stock Market Index fund has returned 1.22% year to date while the Vanguard Total Bond Market Fund has lost 2.97% year to date. The loss in the bond market fund may surprise you, but as interest rates rise, bond values fall, and interest rates have risen meaningfully as of late.

Over the last month, the yield on the 10-year Treasury has risen from around 1% to 1.5%. That may not sound like much, but it is a 50% increase! In theory, a rapid rise in bond yields should also lead to less enthusiasm for stocks, particularly those with low earnings yields. Since low earnings yields translate into high P/Es, in a rising rate environment stocks with the highest P/E ratios should fare worst. Let’s dice up the market and test the theory:

Purity Proves the Point

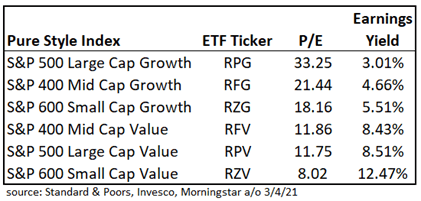

For our rate sensitivity analysis, we will utilize Standard and Poor’s “pure” style indices. These pure style indices isolate the “growth-iest” of the growth stocks and the “value-iest” of the value stocks.

Additionally, Standard and Poor’s constructed these indices for various market capitalizations: S&P 500 for large companies, S&P 400 for mid-size companies, and S&P 600 for small companies. Conveniently, Invesco has issued exchange-traded funds to track each index, making it easy to examine their respective fundamentals and performance.

To begin, let’s sort each of the pure style indices by P/E ratio, highest to lowest. We can also invert those ratios to provide the corresponding earnings yields:

Unsurprisingly, the growth style indices carry higher P/E ratios given their large concentrations in richly-valued technology stocks. For instance, the S&P 500 Pure Growth Index has 40% of its assets in tech compared with only 5% for the S&P 500 Pure Value Index.

Inverting the 33x P/E for the S&P 500 Pure Growth Index derives an earnings yield of 3.01%. A yield this low could and should be problematic as interest rates rise. Currently, AAA corporate bonds yield 2.81% while BBB corporate bonds yield 3.50%, making the average of the two yields 3.15%. When we compare the 3.01% yield of the S&P 500 Pure Growth Index with the 3.15% yield of a comparable corporate bond index, the math actually favors the bonds.

Fortunately, things improve further down the chart.

The pure value indices yield far more than the growth indices, with the S&P 600 Small Cap Pure Value Index yielding a savory 12.47%. Even with corporate bond yields rising over 3%, 12.47% provides an unmistakable competitive advantage for small cap value stocks.

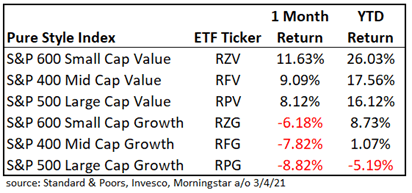

This advantage has not gone unnoticed by investors. Consider the following performance figures over the last month and year-to-date:

Wow!

The S&P 600 Small Cap Pure Value Index has risen 26% year-to-date while the S&P 500 Large Cap Pure Growth Index has lost 5%. Additionally, each of the pure growth style indices has declined over the last month while each of the pure value style indices has risen.

Can this continue?

Well, given the average earnings yield of 9.8% for the pure value indices versus 4.3% for the pure growth indices versus 3.15% for corporate bonds and 1.5% for Treasure bonds, the answer is… yes!