The Full Story:

For those of you who joined us last week for our 2021 investment outlook presentation “The Spoils of War”, you may recall that I concluded my remarks by revealing my deserted island indicator. To qualify as my deserted island indicator, this variable needs to be the one data point that drives them all. For 2021, this indictor isn’t GDP (that’s going to be great), it isn’t corporate earnings (they are going to be superlative), and it isn’t COVID case counts (that’s so 2020). With the government adopting Modern Monetary Theory (MMT), and with stocks highly valued, only inflation threatens this post-COVID party. Subdued inflation can keep the music playing and the markets dancing. Surprise inflation could pull the alarm and send everyone bolting towards the doors. So…given the stakes…it’s time we dig deep into what drives inflation.

Your Inflation Education

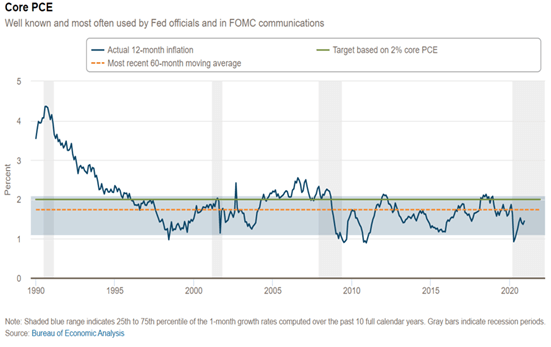

Typing “inflation” into the Fed’s database yields 16,692 different results, including indices like the 5-year, 5-year forward price expectations index and the small arms ammunition price index. If there is an inflation indicator, the Fed tracks it. But the indicator the Fed refers to as “inflation” for setting interest rate policy is the Personal Consumption Expenditures Excluding Food and Energy Chain Price Index, or Core PCE. The Fed asserted in 2012 that they wanted to stabilize Core PCE inflation at 2%. As you can see below, they have struggled to do so. In December, Core PCE inflation sat at 1.5%.

The Bureau of Economic Analysis constructs the PCE index and releases the information monthly with a one-month lag. To calculate inflation, the index tracks prices within a comprehensive basket of consumer goods and services weighted in proportion with household spending patterns. Medical and housing related expenses receive the largest weightings within the basket at 25% and 20% respectively. Service items overall account for 80% of the index, while goods only account for 20%. Goods inflation has been non-existent over the past decade as globalization and digitization have driven down manufacturing and transportation costs. Services inflation has kept price gains aloft thanks to upticks in healthcare, housing and education pricing. Therefore, overall inflation projections amount to price projections across healthcare, housing and education.

Healthcare Headwinds

Reimbursement rates for Medicare and Medicaid largely determine healthcare inflation within Core PCE. These rates have fallen over the last decade as federal, state, and local governments claim a larger share of healthcare spending (now 46%). With Medicare growing twice as fast as overall healthcare spending and political pressure mounting to “cut health care costs”, its hard to project a sharp and persistent upswing in healthcare inflation. Furthermore, the Biden “Rescue America” plan calls for even more centralized healthcare and deep cuts in prescription drug pricing. Healthcare inflation may again exceed headline inflation, but it isn’t returning to its traditional 5%+ levels anytime soon.

Housing Headwinds

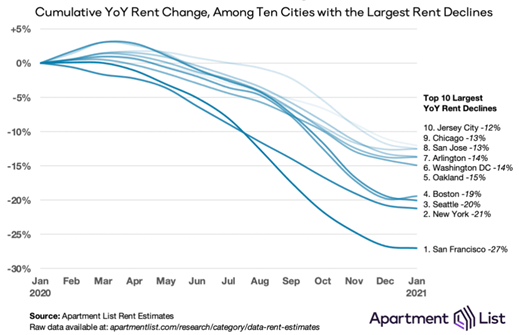

Rent receipts largely determine housing inflation. When unemployment rates climb and rent delinquencies rise, rent inflation falls. Rent inflation averaged close to 4% pre-pandemic and sits at half of that today. With high-cost cities liquidating into low-cost cities given the pandemic fear and the advent of remote work environments, rent price pressures could remain structurally subdued. Consider the collapse in rents across the priciest metro environments:

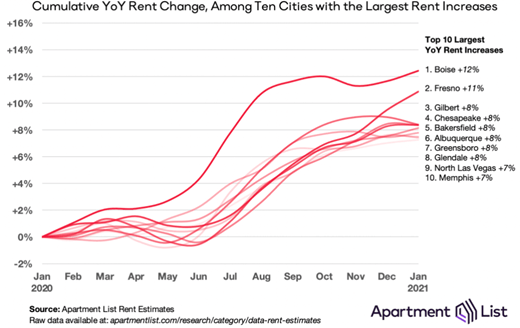

Compare the list above of locations with falling rents and the list below with rising rents. Even after large declines, the average rent in San Francisco is $3,000 a month compared with $1,300 in Boise. Relocating to Boise reduces personal expenses and rent inflation simultaneously.

Tuition Headwinds

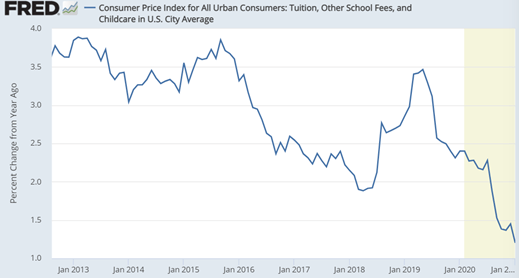

The pandemic led to an historic drop in education costs. Last year, college tuition rates rose at the lowest annual increase on record. With virtual learning environments established, overbuilt college campuses, with their overpriced tuitions, may find themselves competing against far more cost-effective cyber-campuses. Furthermore, many studies have questioned the overall return-on-tuition as student tuition increases have well exceeded wage increases for decades. The chart below demonstrates the accelerating collapse in tuition inflation:

There’s More!

In addition to structural inflation suppressants across healthcare, housing and education, we have other even larger structural headwinds. The broadest measure of US unemployment, the U-6 rate, currently registers 11.1%, 63% higher than pre-pandemic levels of 6.8%. Yet even at that the pre-pandemic level, inflation didn’t rise above the Fed’s 2% rate. There is plenty of slack in the US labor market, and the pending extension of emergency unemployment payments only delays its absorption. Wage inflation isn’t on the horizon. Lastly, the aging of our population, and the accompanying shift in aggregate demand per capita, also weighs on inflation. In fact, this last point apparently concerns the Fed significantly as they pondered it at length during their brainstorming at Jackson Hole last summer. Clearly, the US Fed spends a lot of time thinking about Japan and the negative economic consequences of population declines. The chart below has likely made the rounds at the FOMC.

Taken together, we could see an inflation spike mid-year given the moribund numbers from a year ago, but we do not expect that will dispirit investors. The US has large structural disinflationary forces in play to quell fears of runaway inflation. Overcoming our structural suppressants would require dramatic and sustained growth in US GDP amidst diminishing economic supply. This could happen down the road, but if and until it does, high growth and low inflation will continue to enrich investors.