The Full Story:

Tallying up 2020

The S&P 500 price index rose 16% in 2020 while underlying earnings fell 10%.

How can markets rise when earnings fall?

Market valuation multiples need to rise more than the earnings fall. The P/E ratio for 2020 began at 18x forward earnings and finished at nearly 23x for an expansion of 26%. 26% multiple expansion minus 10% earnings contraction equals 16% gains overall.

Mystery solved!

As we enter 2021, the interest rate peg by the Fed likely correlates with multiples as well. For this market to rise, earnings will have to rise. How high can they go?

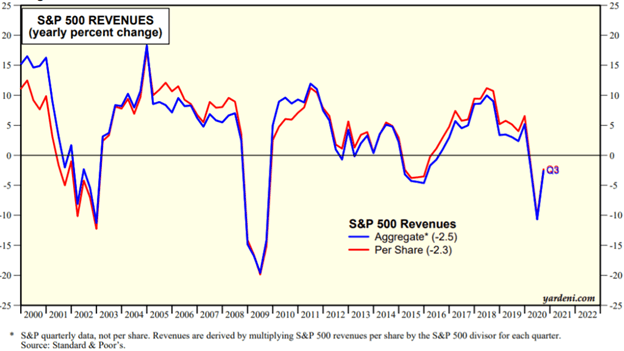

Revenue Preview

Corporate revenue growth correlates with overall economic growth. Global nominal GDP (non-inflation adjusted) should grow by roughly 8% next year. Analysts currently expect S&P 500 corporate revenues to grow 8.2% for 2021.

This week, President-elect Biden announced a $1.9 trillion stimulus plan to tide Americans over until vaccines vanquish COVID-19. $2 trillion equates to roughly 10% of US nominal GDP. He also announced that another spending plan will follow to address infrastructure, climate change, and racial inequality.

We will not see the details of this proposal until February, but given the legislative anchoring around “trillion”, we can safely guestimate another $1 trillion injection.

Oh… and this follows on the heels of the $900 billion passed last month. Even if Biden only gets half of what he’s proposing, the government will inject another 15% into nominal GDP. If that’s the case, 8% revenue estimates for 2021 appear a little light.

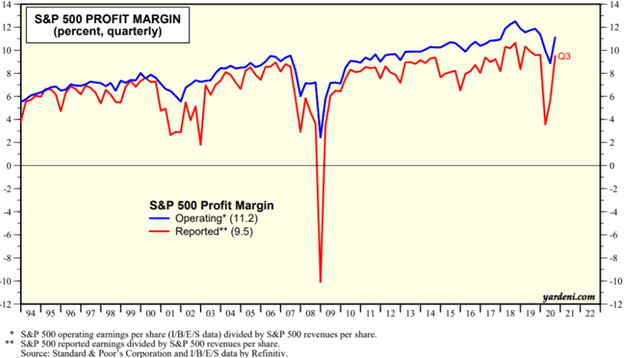

Muscular Profit Margins

Profit margins sink in recessions as business austerity measures lag revenue drawdowns. Reflectively, profit margins surge in expansions as business rescaling measures lag revenue expansions. During the pandemic, businesses purged employees and expenses at a historic rate. The American economy employed 152 million Americans at the end of February 2020. By the end of April, 22 million of these workers had lost their jobs.

In response to COVID-19, it took two months for the American economy to shed 20 million workers. In response to the Great Recession, it took 2 years for the American economy to shed 10 million workers. By the end of December 2020, half of the jobs lost had been regained, leaving 10 million on the sidelines.

For all of 2020, S&P 500 revenues will have fallen 1-2% while total employment across the economy fell 6%. Higher revenues per employee instantly boosts profit margins. Additionally, real estate efficiencies (work from home), commuting efficiencies (travel by Zoom) and financing efficiencies (money for nothing) also add operating leverage.

S&P 500 profits sank 34% in the 2nd quarter and 60% of companies reported lower profit margins vs. a year ago. For the 3rd quarter, profits sank 6% further, but 53% of companies reported margin expansion vs. a year ago. Pre-pandemic profit margins topped out at 12.5%. Analysts predict profit margins will average 10% for 2020 and hit 11% for 2021.

We will keep a watchful eye on 4th quarter profit margins as earnings roll in over the next couple of weeks, but 3rd quarter profit margins hit 11.6%, already above 2021 estimates. We expect profit margins could eclipse record highs within the year.

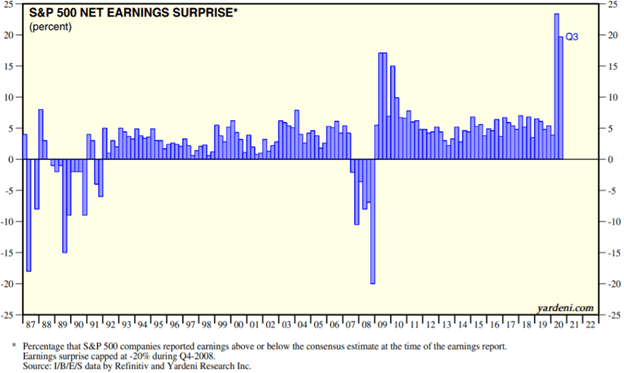

Enthusiastic Earnings

Analysts currently forecast 2021 earnings growth of 22% across the S&P 500 to $168 per share. With nominal GDP underestimated given the Biden Boost of $1.5 to $3 trillion, revenues underestimated given their correlation with nominal GDP, and profit margins underestimated given the beneficial lag between revenue expansion and expense additions, these numbers seem low. Analysts typically underestimate post-recession earnings recoveries by much larger margins than usual as seen in the chart below:

Following the Great Recession in 2009, analysts underestimated earnings growth by 10% for the first year after growth resumed. A 10% undershoot today would project earnings of $185 by year end. That feels a bit aggressive but note in the chart above the historic earnings surprise levels over the last two negative quarters.

Tallying Up 2021!

If the Fed holds rates steady, then the prevailing interest rate environment should anchor rates near these levels. A 10-year Treasury yield anywhere below 2% easily accommodates the current 23x market P/E. Consensus earnings estimates of $168 x a P/E of 23 provide a year–end target of 3864 for the S&P 500, roughly 3% above last year’s close. Should analysts prove conservative by their historic habit of 6%, earnings could approach $180. Multiples may also drift higher as enthusiasm for the recovery builds. For a high side estimate, consider $180 x 25 = S&P 4500, 20% above last year’s close.

In our opinion, upside surprises on GDP, revenues and margins favor the high side. In parlay terms… we’ll take the over.