The Full Story:

Thanks to the rapid and robust response from the US Federal Reserve, the US financial system has remained well lubricated during this COVID crisis. Comments from Fed Chair Powell this week restated his limitless commitment to liquidity. Asset markets of all shapes and sizes rallied in response as gushing money supplies raise water levels beneath all asset prices. But capital ubiquity and availability cannot alone generate economic activity. Businesses’ viability requires revenues. While the Fed’s job has been to flood the markets with cash, its been Congress’ job to flood consumers with cash in compensation for forced unemployment. Therefore, continued COVID revenue restrictions require compensation to keep the economy intact. But now, Congressional constipation has undermined this agreement, and as employment benefits expire, this recession could reinvigorate.

The Worst of Times Becomes the Best of Times

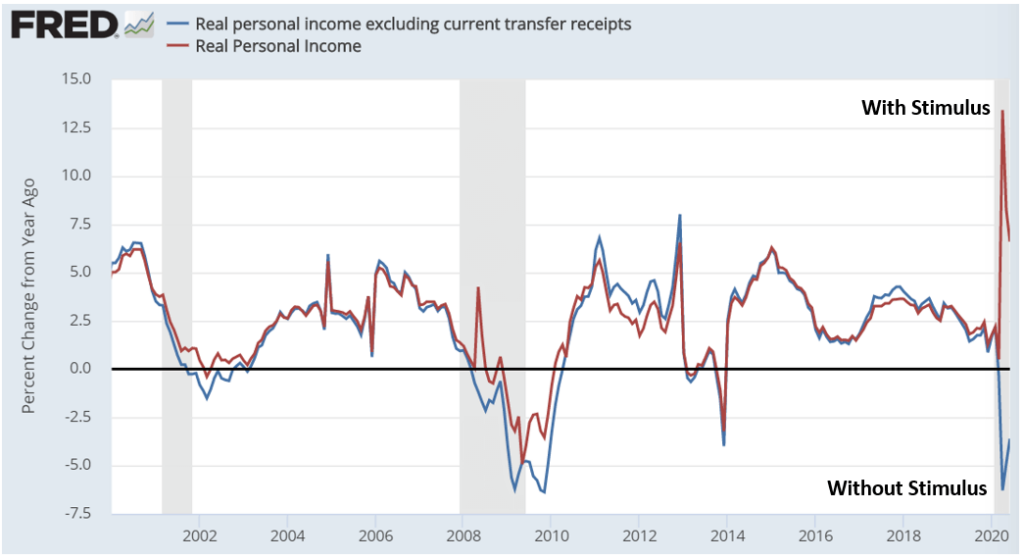

Most believe that the unemployment rate represents the most meaningful coincident measure of an economy’s effectiveness. We associate low unemployment levels with high economic success and high unemployment levels with low economic success. For the most part, I agree. However, in truth, jobs are just a means to an end, and the end is personal income. In normal times, high unemployment levels correspond with low personal income levels. For instance, in 2009 as the US unemployment rate climbed toward 10%, real personal income levels overall dropped 6% year over year. Makes sense – fewer jobs, fewer wages. During the hard stop COVID recession, the unemployment rate spiked to 14.7% while real personal incomes dropped over 7%, a crippling blow for our consumption-oriented US economy. Worst of times! But wait… that personal income number doesn’t account for government transfer payments. Thanks to the rapid and robust fiscal response from Congress, household subsidies including direct payments and enhanced unemployment benefits actually GREW personal incomes, while the unemployment rate rose as seen in the chart below:

Incorporating stimulus, April’s 14.7% unemployment rate actually accompanied an 11% increase in personal incomes overall. In other words, without government support, personal incomes shrank 7%. With government support, personal incomes rose 11%, the highest rate on record. Best of times! This unprecedented effort at income support allowed retail sales to rise and recover record highs even while the household savings rate sits at 20%, also a record high. A COVID crisis met with this level of economic stimulus is almost no crisis at all.

Uncertain Times

Unfortunately, the political will that met COVID with great retaliatory force has dissipated. Partisanship and an election cycle have distracted lawmakers. Nonetheless, a bill appears forthcoming that will extend direct payments to qualified taxpayers and extend unemployment benefits at a reduced rate. The $600 per week federal stipend, over and above a state’s stipend, encouraged people not to work as two thirds of recipients received a raise to stay home. The new $200 a week proposal cuts the total average state and federal unemployment stipend in half. This will certainly incentivize workers to resume work, but they must have workplaces to report to. Most of the displaced workers hail from the leisure and hospitality industries which remain under rolling regulatory interruptions to combat COVID. With the timing and efficacy of a vaccine still uncertain, closures across economic areas of congregation will persist. Studies of the wage parity level for federal unemployment benefits harmonize closer to $400 per week. Should personal incomes including government stipends start shrinking economy wide, this recession will start feeling much more recessionary. Correctly calibrating unemployment stipends with economic closure rates may seem daunting, but it’s also the assignment. This is when we need the best of our lawmakers, not the worst.