The Full Story

Equity markets managed gains on the week despite all of the coronavirus commotion. Economic releases portrayed underlying strength beneath the economy, but a surprise rate cut from the Federal Reserve drove sentiment and interest rates down to eye-watering lows. (As an aside, if you have a mortgage, please stop reading and refinance RIGHT NOW!). While the recent market mayhem may seem chaotic, it has actually been quite orderly. In these modern markets, machines running groupthink algorithms can quickly push prices around as traders feast on volatility and technical activity. However, viewed from afar, these movements, while occasionally overblown, have logical underpinnings. For longer-term investors, big risk reorganizations like this can provide meaningful insights into the overall health of markets and the potential for returns to come. Rather than debate and discuss physical and economic mortality risks this week, let’s take a clinical look at recent market reactions to assess selloff rationale and recovery prognostication.

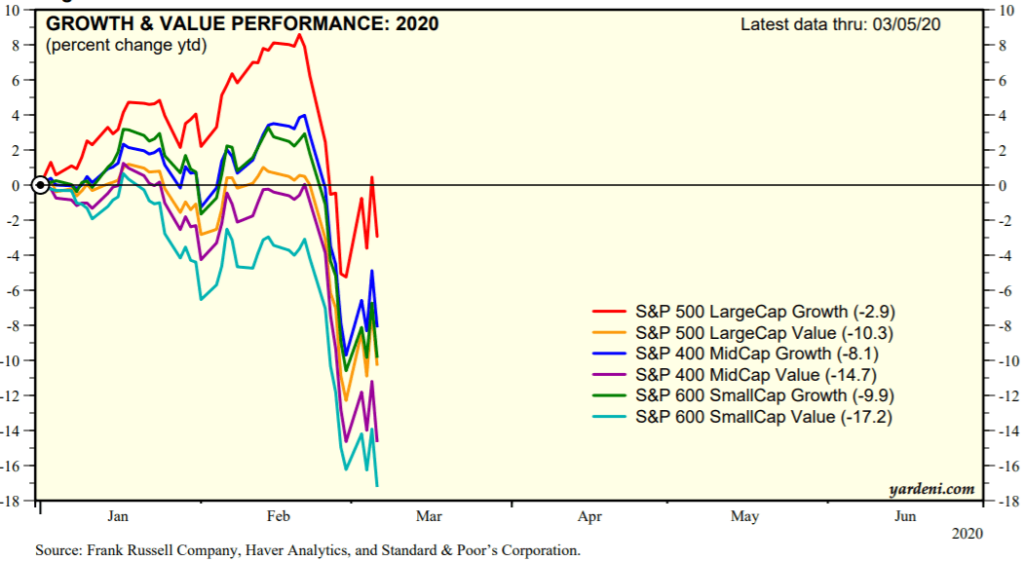

First, let’s examine reactions within the US equity markets. The chart above displays returns across company sizes and investment styles. At the bookends, large-capitalization growth stocks have fallen 2.9% year to date while small-capitalization value stocks have fallen 17.2%. This exaggerated divergence makes sense. If the US economy falls into a panic-inspired recession, cash becomes king, and small companies hold very little cash while large companies like Apple hold ocean freighters full. Furthermore, stocks in economically cyclical industries like financials and consumer discretionary comprise 29% of the S&P 500 large-cap growth index, contrasted with over 51% within the S&P 600 small-cap value index. Analyzing the size and style numbers alone, the US stock market reacted appropriately for the possibility of recession.

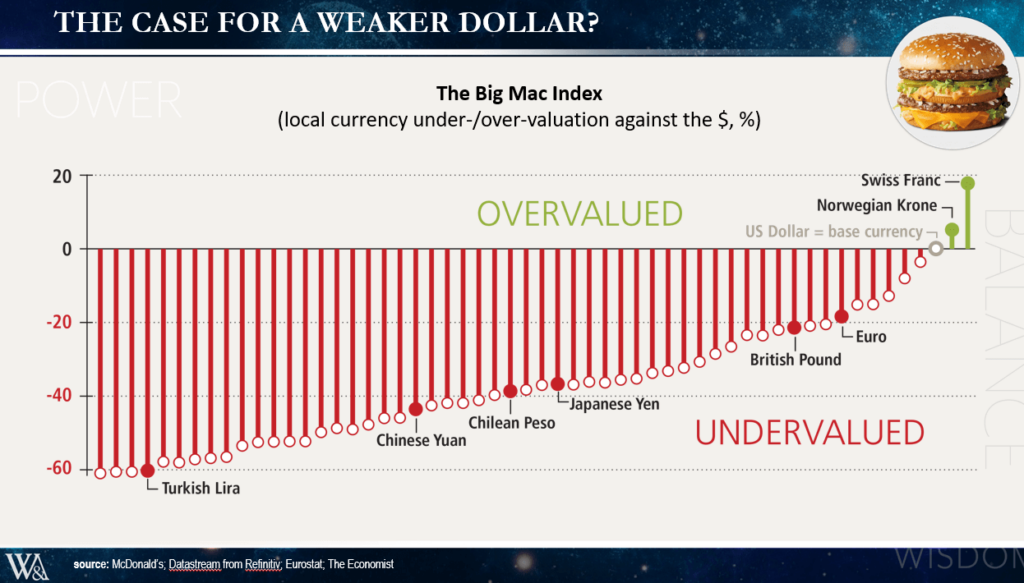

Next, let’s examine geographic returns. This gets very interesting. Before we can start looking at international markets, we must examine the US dollar. Coming into the year, the US dollar appeared overvalued relative to other currencies. The Economist maintains an index comparing the cost of a Big Mac in countries around the world to deduce currency over and undervaluation relative to the US dollar. Here are the current Big Mac index currency value comparisons:

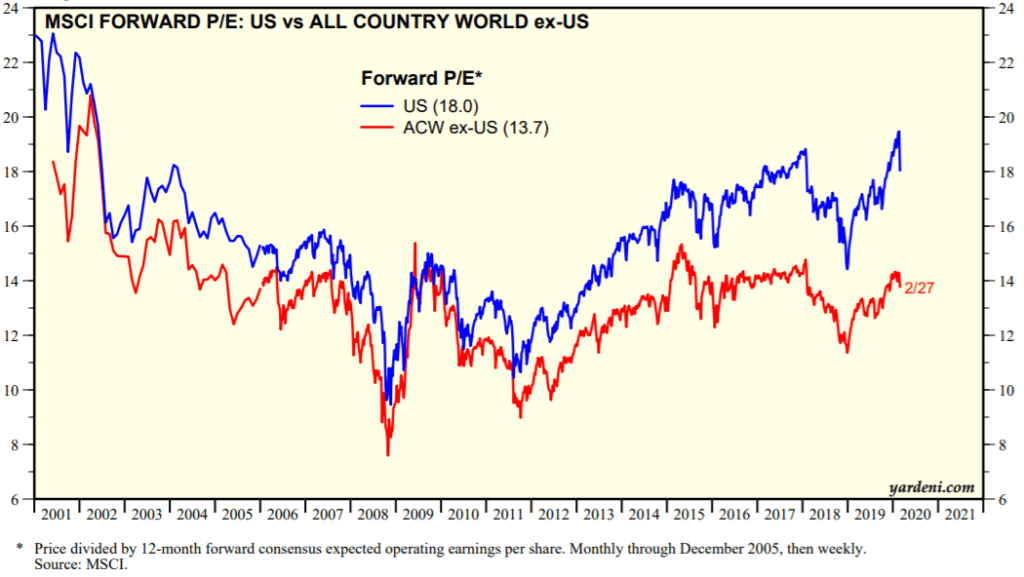

Overall, to quote the Economist, “The Big Mac Index shows currencies are very cheap against the US dollar”. Typically, in times of market stress, the dollar appreciates as fearful foreign money seeks safety within the US. However, over the last month that has not been the case. The DXY dollar index has fallen 4% in the last 12 trading sessions and now stands lower on the year. In fact, the top in the US dollar index occurred back in December of 2016 after nearly a decade of uninterrupted gains. Dollar cycles have significant influence over security prices worldwide, and while a weaker dollar may benefit US companies selling goods abroad, it also rewards US investors owning assets abroad. Let’s see if this logic holds in the current environment. Global stock markets peaked on February 12th. Since then, the MSCI emerging market index has fallen 6.34%, the developed world ex-USA index has fallen 9.03% and the US stock market index has fallen 10.48%. I am not asserting that the decline in the US dollar alone accounts for the outperformance offshore; other factors such as valuation and earnings expectations must also be examined. From a valuation perspective, offshore equities look relatively cheap compared with US equities:

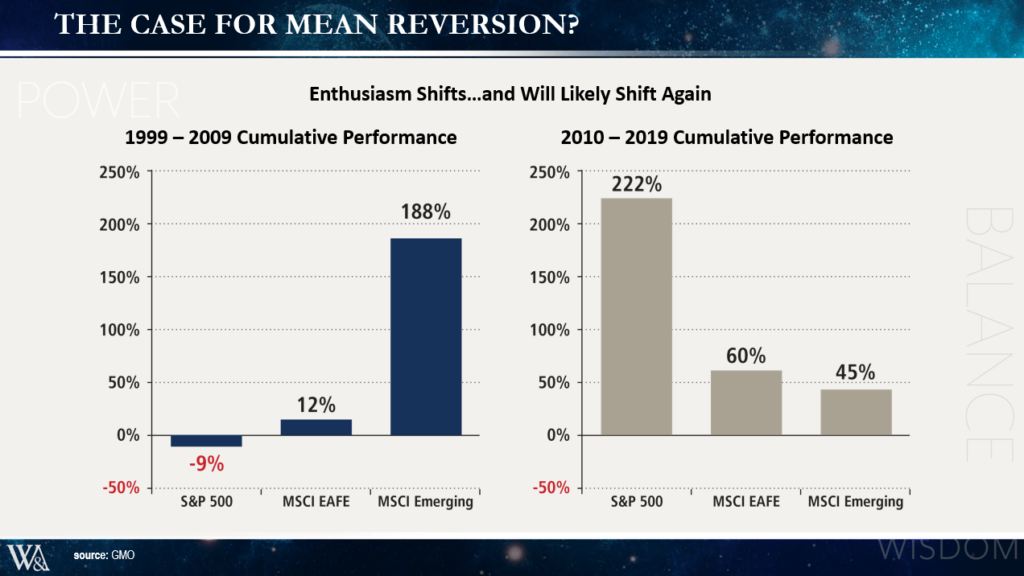

The US trades at 18x forward earnings while the rest of the world trades for 13.7x, for a discount of 25%. From an earnings perspective, analysts currently project earnings growth of 19.5% for US companies over the next two years. This compares with 20.6% for Europe and 28.7% for the emerging markets. These numbers will fall as the consequences of the coronavirus register, but they should fall somewhat proportionately given the global nature of the crisis. To summarize, the combination of currency, valuation and earnings growth advantages have led to outperformance for offshore markets since global indices peaked on February 12th. The atypical outperformance of offshore currencies and offshore markets during this time of stress may foretell continued outperformance should the stress recess. If you believe in mean reversion, the chart below should tickle your contrarian senses. I’ll end this discussion with the picture rather than a thousand words!